Amazon Prime Day 2026: $26.4 Billion in Sales, a Fatigued Consumer, and What Every Retailer and CPG Brand Needs to Know

The numbers are record-setting again. But look past the headline and you will find a more complicated story about consumer behavior, promotional saturation, and who actually won Prime Day 2026.

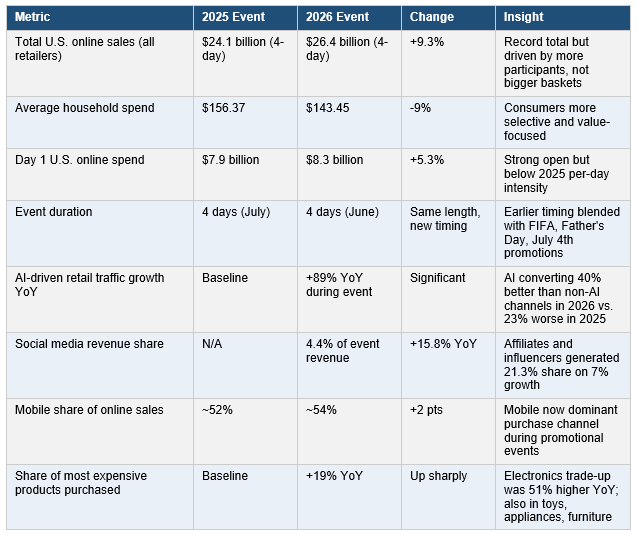

Amazon Prime Day 2026 ran June 23 through June 26, marking the first time the event moved from its traditional July window to June, extending the event from two days to four for the second consecutive year. By the headline measure, it was another record: total U.S. online retail spending during the four-day period reached $26.4 billion, according to Adobe Analytics, representing a 9.3% increase over the comparable prior-year period. Day one alone generated $8.3 billion in U.S. online spend, up 5.3% from day one of the 2025 event. For context, the $26.4 billion total now exceeds the combined U.S. online spending on Black Friday and Cyber Monday, making Prime Day the single largest annual online shopping event in the country. And yet the 2026 results contain signals that are considerably more nuanced than the headline suggests, and those signals matter deeply for CPG brands, retailers, and anyone making decisions about promotional strategy in the second half of the year.

The first important nuance is that per-household spending declined. Adobe Analytics data shows that average household spend during the 2026 event fell 9% year over year, dropping from $156.37 to $143.45. The total spending record was set not because individual households spent more, but because more households participated in the event overall. That distinction is meaningful. A consumer who shows up to buy exactly what they planned to buy at a price they were waiting for is a fundamentally different customer than a consumer who got swept up in promotional energy and added items to their basket. Retail analyst Sonia Lapinsky of AlixPartners described this dynamic concisely to Reuters, noting that consumers were stocking up on products they were going to buy anyway, and characterizing the underlying consumer as fatigued. Circana chief retail adviser Marshal Cohen reinforced that read, observing that across multiple major promotional weeks this year, the potency of these events has been waning as the promotional calendar becomes increasingly compressed.

Chart: Amazon Prime Day 2026 headline results and key consumer behavior metrics compared to prior year, sourced from Adobe Analytics, Numerator, and Circana.

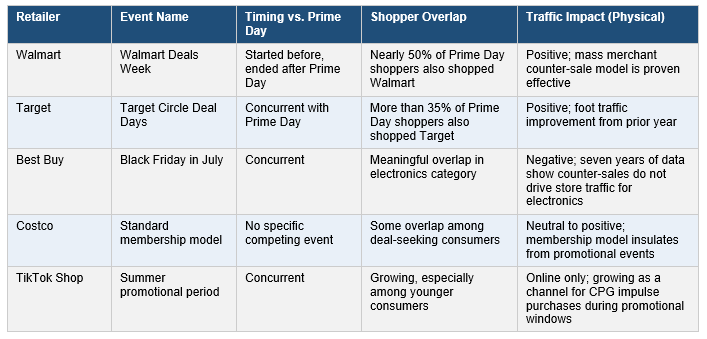

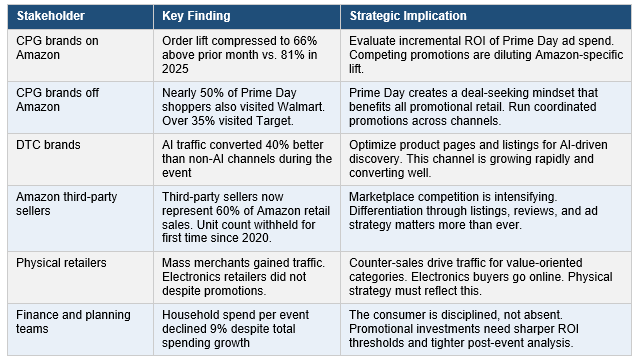

The competitive landscape around Prime Day 2026 was more crowded than any prior year. Target ran its Circle Deal Days concurrently. Walmart extended its Deals event to a full week, starting before Prime Day began and running past it. Best Buy, Kohl’s, and Staples all launched simultaneous promotions. The result was that nearly half of all Prime Day shoppers also shopped Walmart Deals during the same period, and more than a third shopped Target Circle Week. For CPG brands and Amazon third-party sellers, this cross-retailer shopping behavior has a direct financial consequence: order lifts on Amazon were measurably lower than in prior years. Data from Incrementum Digital, which works with approximately 100 brands, showed client sales improving 66% versus the prior month during the event period, down from an 81% improvement in the comparable prior-year period. The likeliest explanation is comparison shopping across simultaneous promotions, which diluted the concentrated buying pressure that defined earlier Prime Day events when Amazon had the promotional calendar largely to itself.

The AI-driven traffic data from this year’s event is among the most strategically significant findings in the entire dataset. Adobe Analytics tracked a 235% year-over-year increase in traffic from AI sources to U.S. retail sites from January through May 2026. During the Prime Day event window, AI-driven traffic grew 89% year over year. More importantly, the conversion behavior of that AI-driven traffic reversed dramatically from 2025. In the 2025 event, AI traffic converted 23% worse than non-AI channels. In 2026, AI traffic converted 40% better than non-AI channels. That is a 63-percentage-point swing in relative conversion performance in a single year, and it reflects the rapid maturation of AI shopping tools from novelty to utility. Consumers who arrive at a retail site via an AI recommendation are increasingly arriving with high purchase intent, specific product knowledge, and lower price sensitivity than the average paid search or social media-driven visitor.

Chart: Prime Day 2026 competitive retail landscape, showing how competing promotional events and cross-retailer shopping affected the overall event dynamics.

For third-party sellers on Amazon, the 2026 event produced solid but moderating results against a backdrop of increasing marketplace competition. Third-party sellers now account for approximately 60% of total Amazon retail sales, meaning the majority of Prime Day transactions flow through the marketplace rather than Amazon’s own first-party inventory. Amazon withheld the specific unit count for the first time since 2020, having previously disclosed 375 million units sold in 2023 and over 300 million in 2022. That omission is notable. What the company did confirm is that independent sellers achieved record sales and a record number of items sold, language that is consistent with volume growth but avoids specific quantification. For brands managing Amazon as a channel, the practical implication of the 2026 results is clear: Prime Day remains the single highest-volume selling period of the year, but the lift above baseline is compressing as more brands participate, advertising costs rise, and consumers spread their promotional shopping across a broader set of retailers and events.

The category-level data from Adobe reveals a consumer who was willing to trade up on certain planned purchases but was not engaging in the kind of broad discretionary spending that characterized the earlier Prime Day events of 2021 and 2022. The share of the most expensive products purchased across the event increased 19% year over year, with electronics trade-up the most pronounced at 51% higher than the prior year. Toys, appliances, and furniture also saw meaningful trade-up behavior. This pattern is consistent with what analysts call the deal-stacking consumer: a shopper who has been waiting to make a specific higher-ticket purchase, using a promotional event as the trigger and price discount as the justification. Back-to-school categories performed well, with kids items, apparel, and personal hygiene also among the top performing segments. These results reinforce the positioning of Prime Day as an event that functions partly as the unofficial start of the back-to-school season for a large segment of U.S. households.

The promotional timing context also matters for interpreting the results. Telsey Advisory Group analysts noted that Prime Day 2026 shifted two weeks earlier than usual and blended with multiple retail promotional moments including Memorial Day, FIFA World Cup events, Father’s Day, and the Independence Day and America 250 celebrations. That clustering of promotional intensity into a single extended midyear window created a period of elevated consumer spending that is difficult to attribute cleanly to any single event. Out of 68 retailers and brands analyzed by Telsey, 40% were running more promotional activity than in the prior year during this period. For CPG brands evaluating the ROI of their Prime Day promotional investments, this context is essential: the sales lift attributable to Prime Day specifically is harder to isolate in an environment where consumers are being pulled simultaneously by competing offers from a dozen different directions.

Chart: Key takeaways from Prime Day 2026 organized by stakeholder and their strategic implications.

Bottom Line: Amazon Prime Day 2026 set another total sales record, and that record deserves context. Household spending declined, promotional fatigue is measurable, competing events diluted Amazon-specific lift, and the consumer showing up to these events is buying what they planned to buy at a price they were waiting for. That is not a weak consumer. It is a strategic one. CPG brands and retailers that understand the difference will build better promotional plans for the second half of the year than those that read the headline number and assume the same playbook will keep working.