IEEPA Tariff Refunds: The Tax Treatment Every Retail and CPG Finance Team Must Understand Now

A tariff refund is not free money. It is a taxable event, and the mechanics depend on how your business recorded the original duty payments.

On February 20, 2026, the U.S. Supreme Court issued its ruling in Learning Resources, Inc. v. Trump, determining that the International Emergency Economic Powers Act did not authorize the tariffs imposed under its framework. The decision triggered a refund obligation for approximately $166 billion in duties collected from roughly 330,000 importers who paid IEEPA tariffs between February 2025 and February 2026. U.S. Customs and Border Protection launched the CAPE refund system on April 20, 2026, and refunds have been processing at a pace CBP estimated at 60 to 90 days per claim. For mid-sized retail and CPG importers, individual refund checks are running in the range of $1 million to $10 million. At those figures, the tax treatment is not a footnote in the year-end close. It is a material financial event that requires careful planning before the cash arrives.

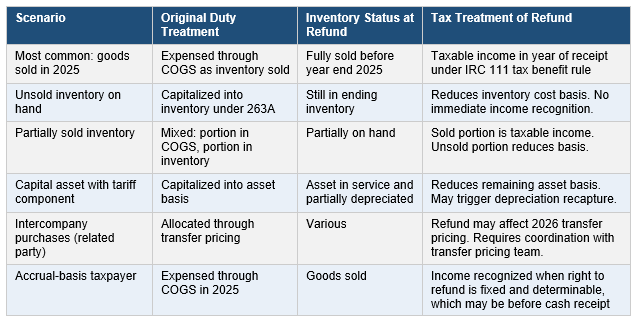

The central tax principle governing IEEPA tariff refunds is the tax benefit rule, codified in IRC Section 111. The rule holds that a recovery of a previously deducted item is includible in gross income to the extent the original deduction reduced the taxpayer’s tax liability in the prior year. Applied to tariff refunds, the analysis turns on a single question: has the duty payment already produced a tax benefit? For most retail and CPG businesses that flow tariff costs through cost of goods sold as inventory is sold, the answer for duties paid in 2025 on goods that were sold before year end is yes. Those duties reduced taxable income in 2025, and the refund is therefore taxable income in 2026, the year of receipt for cash-basis taxpayers and potentially 2026 as well for accrual-basis taxpayers whose right to the refund became fixed and determinable upon CBP acceptance of their CAPE Declaration.

Chart: IEEPA tariff refund tax treatment decision tree by inventory status and accounting method.

LIFO taxpayers face additional complexity. Tariff costs embedded in prior LIFO layers that have already been relieved into cost of goods sold may require analysis that coordinates the tax benefit rule with the LIFO methodology under IRC Sections 471 and 472. The question is whether the refund relates economically to historical layers that have already produced a tax benefit. Firms with LIFO inventory and significant IEEPA tariff exposure should engage qualified tax counsel before the refund posts to their books, because the mechanical answer is not always the same as the economically correct answer.

The interest component of the refund requires separate treatment. Statutory interest paid by the government on refunded duties is ordinary income in the year received and is not eligible for any COGS reduction treatment. Accrual-basis taxpayers may need to separately track the timing of when interest becomes fixed and determinable from the timing of the principal refund. For multinational businesses, PwC has estimated that approximately half of the potential IEEPA refunds relate to intercompany transactions, raising transfer pricing questions about which entity is entitled to the refund, whether the intercompany pricing arrangements need to be revisited, and what disclosure obligations apply. These questions should be addressed before the cash is distributed within the corporate group, not after.

The GAAP accounting treatment runs in parallel with the tax analysis and may create timing differences that affect deferred tax balances. Under the loss recovery model, which applies when recovery is probable based on the Supreme Court ruling and CBP acceptance of the CAPE Declaration, companies recognize a receivable and reduce COGS in the period the recovery becomes probable, regardless of when cash is received. Under the gain contingency model, recognition is deferred until CBP formally approves and reliquidates the entries. The choice between these models requires professional judgment and documentation, and the timing difference between GAAP recognition and taxable income can create deferred tax asset or liability positions that need to be reflected in the quarterly close.

Bottom Line: The IEEPA tariff refund is a genuine and potentially large cash recovery for retail and CPG importers. It is also a tax event that requires advance planning. The businesses that understand the tax benefit rule, coordinate their inventory accounting with their tax analysis, and address transfer pricing implications before the refund arrives will have a cleaner close and a smaller surprise in their 2026 provision. Those that treat it as found money and figure out the tax later will not.