IRS Raises the Standard Mileage Rate to 76 Cents Per Mile Effective July 1, 2026

Fuel costs rose 38% in the first half of 2026. The IRS responded with a rare mid-year rate adjustment. Here is what changed, what the depreciation recapture component means, and what you need to do.

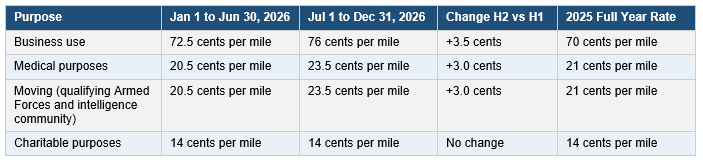

The IRS issued Announcement 2026-11, published in Internal Revenue Bulletin 2026-29 on July 9 and dated July 13, 2026, increasing the optional standard business mileage rate from 72.5 cents per mile to 76 cents per mile for all business miles driven on or after July 1, 2026. The change applies to cars, vans, pickups, and panel trucks regardless of fuel type, covering electric, hybrid-electric, gasoline, and diesel vehicles equally. The American Automobile Association reported that the average price for regular gasoline rose from $2.819 per gallon on January 8 to $3.890 per gallon on July 15, an increase of approximately 38%, which the IRS cited as the direct driver of the adjustment. Mid-year rate changes are rare. The last comparable adjustment was in 2022.

Because the original rate of 72.5 cents remains in effect for January 1 through June 30, 2026, this year now carries two standard business mileage rates. The rate that applies is determined by the date the miles were driven, not the date the reimbursement is processed or paid. Expense reports, accountable plan reimbursements, and tax deduction calculations must all reflect the correct rate for the period in which the miles occurred.

Chart: 2026 IRS standard mileage rates by purpose and period, with prior year comparison.

There is a component of the standard mileage rate that most business owners and even some CPAs overlook: the portion of each mile driven that the IRS treats as depreciation rather than as a current operating expense. Under IRS Notice 2026-10 and the rules established in Rev. Proc. 2019-46, a defined portion of the business standard mileage rate is characterized as the depreciation allowance for the vehicle. For 2026, that depreciation component is 35 cents per mile, up from 33 cents per mile in 2025 and 30 cents per mile in 2024. This matters because of what happens when the vehicle is eventually sold.

When a taxpayer sells or otherwise disposes of a vehicle for which the standard mileage rate has been used in prior years, the IRS requires that the vehicle’s adjusted tax basis be reduced by the cumulative depreciation component from all years the standard mileage rate was claimed. This basis reduction affects the gain or loss recognized on the sale, and any gain attributable to the depreciation deductions previously taken is subject to Section 1245 ordinary income recapture, taxed at ordinary income rates rather than at the preferential capital gains rate. A business owner who has driven 50,000 business miles using the standard mileage rate in 2026 alone must reduce the vehicle’s basis by $17,500 (50,000 miles multiplied by the 35 cent depreciation component) for purposes of calculating gain on an eventual sale.

The recapture calculation is straightforward but frequently missed when a vehicle is sold or traded in. If a business owner purchased a vehicle for $40,000 in 2023 and has used the standard mileage rate exclusively for four years, accumulating $25,200 in deemed depreciation through the depreciation component of the rate, the adjusted basis at the time of sale is $14,800. If the vehicle sells for $22,000, the $7,200 gain is all Section 1245 recapture taxed as ordinary income, not capital gain. For a taxpayer in the 32% bracket, the after-tax difference between ordinary income treatment and long-term capital gains treatment on that $7,200 is approximately $720. For a business owner who has accumulated significantly more mileage over many years, the recapture exposure on a vehicle sale can be considerably larger and deserves attention before the sale is executed.

Bottom Line: Update your reimbursement systems to apply 76 cents per mile for all business mileage driven on or after July 1. For any vehicle that has been using the standard mileage rate, keep a running total of the depreciation component by year so the adjusted basis is accurate when the vehicle is eventually sold. The recapture on disposal is ordinary income and is often a surprise to both the business owner and the tax preparer when it surfaces at the time of the sale.