Kroger Acquires Giant Eagle and What the Biggest Retail & CPG Deals of 2026 Mean for Your Business

Grocery consolidation is accelerating, megadeals are back, and the competitive landscape is being redrawn. Here is what every retail and CPG operator needs to understand.

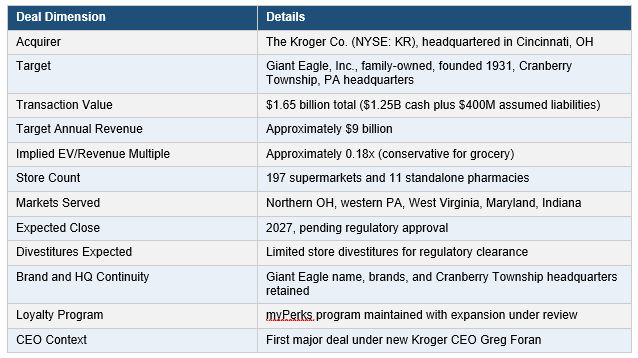

Breaking: Kroger Acquires Giant Eagle for $1.65 Billion

On July 1, 2026, Kroger announced a definitive agreement to acquire Giant Eagle, Inc., the Pittsburgh headquartered family-owned grocery chain, for $1.65 billion. The purchase price includes $1.25 billion in cash consideration and the assumption of approximately $400 million in outstanding liabilities. The deal has been unanimously approved by Kroger’s Board of Directors and is expected to close in 2027, pending regulatory approval and limited store divestitures. The transaction marks Kroger’s first major acquisition under newly appointed CEO Greg Foran and its first significant M&A move since the failed $25 billion Albertsons merger collapsed in 2024.

Giant Eagle is a significant regional grocer by any measure. Founded in 1931 and ranked among Forbes’s largest private corporations, the company operates 197 supermarkets and 11 standalone pharmacies across northern Ohio, western Pennsylvania, West Virginia, Maryland, and Indiana. It generates approximately $9 billion in annual sales and is one of the most respected regional food retailers in the country, with a strong reputation in pharmacy, private label, fresh foods, and customer loyalty. That loyalty is anchored by its myPerks program, which Kroger has confirmed it intends to maintain and potentially expand.

Chart: Kroger and Giant Eagle deal overview showing transaction structure, strategic rationale, and key operational facts.

The strategic logic of the deal is clear. Giant Eagle gives Kroger a meaningful footprint in adjacent markets, most notably the Pittsburgh metropolitan area where Kroger has historically had limited presence, and fills geographic gaps in the Upper Midwest and Mid-Atlantic region that the Albertsons deal would have addressed at far greater scale and cost. At 0.18x revenue, the purchase price reflects the thin margin realities of conventional grocery retail. The assumption of $400 million in liabilities suggests Giant Eagle carries meaningful real estate and debt obligations consistent with a large multi-state brick and mortar operator.

From a financial modeling perspective, the deal raises several questions that CPG suppliers, retail operators, and competitive grocers in the affected markets will be working through over the coming months. For CPG brands that sell into Giant Eagle today, the acquisition signals a change in buying structure and category management leadership that will likely take 18 to 24 months to fully manifest. Kroger’s private label program is one of the most aggressive in conventional grocery and will eventually be integrated into Giant Eagle’s assortment, creating incremental shelf pressure for branded CPG suppliers in those markets. Brands that are currently well positioned on Giant Eagle’s shelves should proactively assess their vulnerability to private label displacement in the post-integration period.

For regional grocery competitors in the affected markets, including Aldi, Giant Food (unrelated), Meijer, and independent operators, the arrival of Kroger’s operational and procurement scale in these geographies will increase competitive intensity across pricing, loyalty infrastructure, and assortment depth. Retailers in overlapping markets should evaluate their price positioning, loyalty program effectiveness, and supplier relationships before the integration is complete and Kroger’s full operational advantages are deployed.

2025 and 2026 Retail & CPG M&A: The Biggest Deals and What Is Driving Them

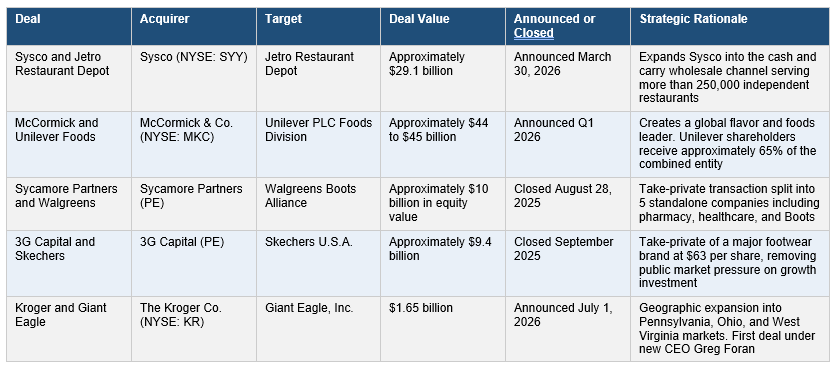

The Kroger and Giant Eagle transaction does not exist in isolation. The past twelve months have seen a dramatic resurgence in large-scale retail and CPG deal making, reversing the M&A slowdown of 2024 and producing some of the largest consumer industry transactions in years. Several forces are converging to drive this activity. Cost pressures from tariffs and inflation are making scale more economically valuable. Consumer demand is shifting in ways that favor acquisition over organic repositioning. Private equity has returned to the sector with significant appetite for large-cap retail assets. The result is a reshaping of the competitive landscape that will affect market structure, supplier relationships, and category economics for years to come.

Chart: Major U.S. retail and CPG mergers and acquisitions from 2025 through July 2026.

The Sysco and Jetro Restaurant Depot deal, announced March 30, 2026, is the largest food distribution transaction in recent memory. Valued at approximately $29.1 billion and including $21.6 billion in cash and 91.5 million Sysco shares, the acquisition gives Sysco direct ownership of the cash and carry wholesale model that Jetro has pioneered across 166 warehouse locations in 35 states. Sysco is already the nation’s largest foodservice distributor. The deal’s significance for CPG and food brands is considerable because Jetro has historically served as a price checking mechanism for independent restaurants, who used it as an alternative to Sysco’s broadline pricing. With Jetro inside Sysco, that competitive dynamic changes fundamentally. Credit agencies reacted cautiously, with both Fitch and Moody’s placing Sysco on rating watch following the announcement due to the significant debt burden of the transaction.

The McCormick and Unilever Foods merger is the most strategically ambitious CPG deal of the cycle. McCormick, with a market capitalization of approximately $14 billion, is combining with Unilever’s Foods division, which is home to brands including Hellmann’s, Knorr, Marmite, and Colman’s. The transaction is valued at approximately $44 to $45 billion. The combined entity, in which Unilever shareholders will retain approximately 65% ownership, would create a global flavor and branded foods platform at a scale that changes competitive dynamics across grocery and foodservice channels worldwide. For CPG brand operators and retailers, the emergence of a significantly larger branded foods competitor with McCormick’s flavor expertise and Unilever’s distribution scale warrants close monitoring.

The private equity transactions reflect a broader pattern identified by McKinsey. Sycamore’s take private of Walgreens at approximately $10 billion and 3G Capital’s $9.4 billion acquisition of Skechers are part of a broader shift in which PE firms have moved their focus from CPG targets to large-cap retail assets, with average deal sizes more than doubling between 2024 and 2025. Both deals remove major retail brands from public market scrutiny, giving new ownership teams the ability to restructure operations, close underperforming locations, and reposition the businesses without quarterly earnings pressure. For CPG brands that sell into Walgreens, now split into five standalone companies, the organizational fragmentation of the buyer relationship is a real and immediate operational challenge.

What This Wave of M&A Means for Retail Operators and CPG Brands

The consolidation wave underway in retail and CPG has direct financial and strategic implications for operators at every scale. For CPG suppliers, the consolidation of retail buying power accelerates a trend that was already well established: fewer and larger buyers with more sophisticated procurement teams, more aggressive private label programs, and less tolerance for brands that cannot demonstrate clear consumer demand. As Kroger integrates Giant Eagle, as Sysco integrates Jetro, and as the McCormick and Unilever combination takes shape, the category management conversations, pricing negotiations, and promotional calendars that CPG brands manage will shift in ways that require proactive relationship and portfolio management.

For finance teams at companies of all sizes, the current M&A environment reinforces the importance of scenario planning that accounts for structural changes in the competitive landscape. The assumptions underlying a three-year financial plan built before the Sysco and Jetro merger, the McCormick and Unilever combination, and the Kroger and Giant Eagle deal are materially different from the assumptions that should underlie one built today. Market structure, buyer concentration, distribution dynamics, and competitive intensity have all shifted. Financial plans that do not reflect these changes will generate surprises that could have been anticipated with more current inputs.

Bottom Line: The consolidation wave reshaping retail and CPG is not a background event. It is an active force changing who your buyers are, who your competitors are, and what your margins will look like in the next two to three years. The businesses that understand and plan for these structural shifts now will be better positioned than those that react to them after the fact.