No Tax on Tips and Overtime: What Retail Employers Must Do Before the Next Payroll Cycle

The OBBBA created a meaningful tax break for your hourly workforce. Your payroll system, W-2 reporting, and HR communications may not reflect it yet.

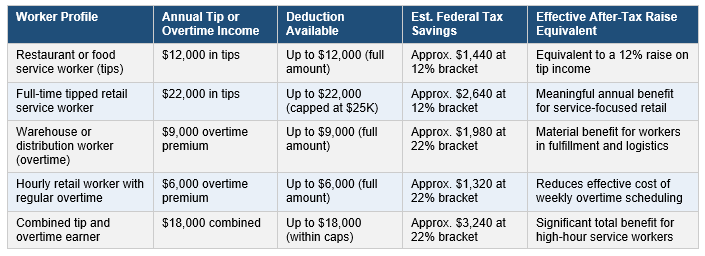

The One Big Beautiful Bill Act introduced two new individual income tax deductions that are directly and materially relevant to the retail industry: a deduction of up to $25,000 for qualified tip income and a deduction of up to $12,500 per year for the premium portion of overtime pay. Both provisions are available for tax years 2025 through 2028. Both carry income phase-outs beginning at $150,000 of modified adjusted gross income for single filers and $300,000 for married filing jointly. And both create compliance, reporting, and communication obligations for employers that go well beyond simply knowing the rules exist.

The tip deduction applies to employees who receive tips in the ordinary course of employment in industries where tipping is customary. The IRS has confirmed that this includes food service, restaurant, and hospitality-adjacent retail. The deduction applies to qualified tips as defined under the existing tip reporting framework and is taken by the employee on their individual return, not by the employer. However, the employer’s W-2 reporting of tip income in Box 7 and Box 1 is the foundation on which the employee builds the deduction. Errors or inconsistencies in employer reporting of tip income will create discrepancies between the employee’s W-2 and their claimed deduction, increasing the likelihood of IRS correspondence and audit exposure for both the employee and the employer.

Chart: Tip and overtime deduction parameters and illustrative after-tax income impact for common retail workforce profiles.

The overtime deduction is technically a deduction for the premium portion of overtime pay, which is the incremental amount above the regular hourly rate that federal law requires for hours worked beyond 40 per week. It is not a deduction for the entire overtime paycheck. An employee who earns a regular rate of $20 per hour and receives $30 per hour for overtime is eligible to deduct only the $10 premium, not the full $30. Employers should ensure that their payroll systems are capable of separately identifying and reporting the premium component of overtime pay in a format that supports the employee’s ability to document the deduction on their individual return.

The employer compliance obligations span three distinct areas. First, payroll system configuration: systems must correctly identify qualifying tip income and overtime premium pay in a way that facilitates accurate W-2 reporting. Second, written information and employee communication: workers who are unaware of the deduction cannot claim it, and failing to inform a workforce of a meaningful tax benefit they are entitled to is both a missed retention opportunity and a potential labor relations issue. Third, HR policy review: for employers who have historically discouraged or limited overtime to control labor costs, the reduced after-tax cost of overtime for hourly workers changes the calculus on how aggressively to manage overtime hours versus how to use the benefit as a workforce retention tool, particularly in the current labor market.

Bottom Line: The no-tax-on-tips and overtime deductions are individual tax benefits that land squarely on the employer’s compliance desk. Update your payroll systems, communicate the benefit to your workforce before the next filing season creates confusion, and evaluate whether the reduced after-tax cost of overtime changes your labor scheduling strategy. The benefit is real, the workforce will eventually find out about it, and the employer who tells them first earns the credit.