Raw Material Volatility Is Becoming the New Normal

Commodity prices will keep swinging. Is your margin model built for it?

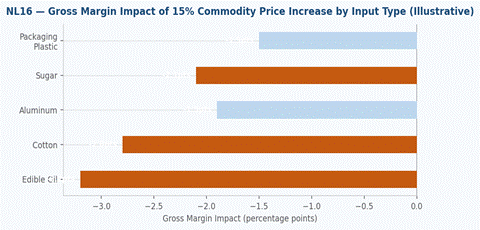

Raw material costs continue to fluctuate meaningfully across retail and CPG categories, driven by a combination of geopolitical instability, climate-related supply disruptions, energy price movements, and shifting demand patterns. Key inputs including sugar, edible oils, cotton, aluminum, plastics, and packaging materials have each experienced significant price swings in recent years — and there is little reason to expect that dynamic to stabilize in the near term.

The operational challenge is not simply cost levels — it is unpredictability. A sudden 15% spike in a key input can compress gross margins before pricing adjustments can be communicated to retail partners or pushed through to consumers. This is particularly acute for companies locked into fixed retailer pricing agreements or promotional calendars that do not allow for rapid cost pass-through.

Chart: Estimated gross margin impact (in percentage points) of a 15% commodity price increase by key input type.

Finance teams should work closely with procurement leaders to evaluate hedging strategies where available, explore supplier contracts with indexed pricing provisions, and assess the value of diversifying across multiple supply sources. Overreliance on a single supplier introduces both pricing risk and operational risk simultaneously.

Sensitivity analysis around key commodity inputs should be a standard component of quarterly forecasting. Companies that regularly model how raw material price movements affect EBITDA are significantly better positioned to respond quickly — whether through pricing adjustments, promotional changes, or cost reduction initiatives elsewhere in the business.

Bottom Line: Commodity volatility is likely to remain a persistent feature of the environment. Proactive sourcing strategy and pricing discipline are the most effective defenses.