The QBI Deduction Is Now Permanent — What Pass-Through Businesses Should Do Next

Pass-through owners got a permanent tax break. Are you capturing it fully?

One of the most consequential recent tax developments for privately held retail and CPG businesses is the permanent extension of the Section 199A Qualified Business Income (QBI) deduction. Previously set to expire after 2025, the deduction has been made permanent under recently enacted legislation — creating a more stable and predictable planning environment for the large share of retail and consumer product businesses structured as pass-through entities.

The QBI deduction allows eligible pass-through businesses — including S-corporations, partnerships, and single-member LLCs — to deduct up to 20% of qualified business income, effectively reducing the federal tax rate on that income. The legislation that made the deduction permanent also expanded the income thresholds at which phase-in limitations begin to apply, allowing a broader population of business owners to access the full deduction before W-2 wage and qualified property limitations take effect.

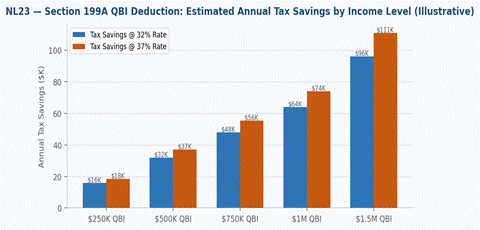

Chart: Estimated annual federal tax savings from the Section 199A QBI deduction at 32% and 37% marginal rates, by income level.

To illustrate the benefit: an S-corporation generating $750,000 in qualified business income could potentially reduce taxable income by $150,000 through the deduction, producing substantial federal tax savings depending on the owner’s marginal rate. The magnitude of that benefit makes entity structure, compensation planning, and income timing decisions far more consequential than they might otherwise be.

Business owners should now revisit entity structure, owner compensation strategy and W-2 wage optimization, income timing and year-end planning decisions, and expansion and reinvestment structures that preserve qualified business income. The permanence of the deduction also has implications for larger strategic decisions — including whether converting to C-corporation status makes sense, how acquisitions should be structured, and how owner distributions should be timed relative to income recognition.

Bottom Line: A permanent QBI deduction creates meaningful and durable tax planning opportunities. Now is the time to make sure your structure and strategy are optimized to capture them.